New Study Finds Strong Natural Gas Market That Can Meet Domestic and Export Demand at Low Prices

Policy Reform on Permitting and Infrastructure are Critical to Bringing Lowest Cost Resources to Market

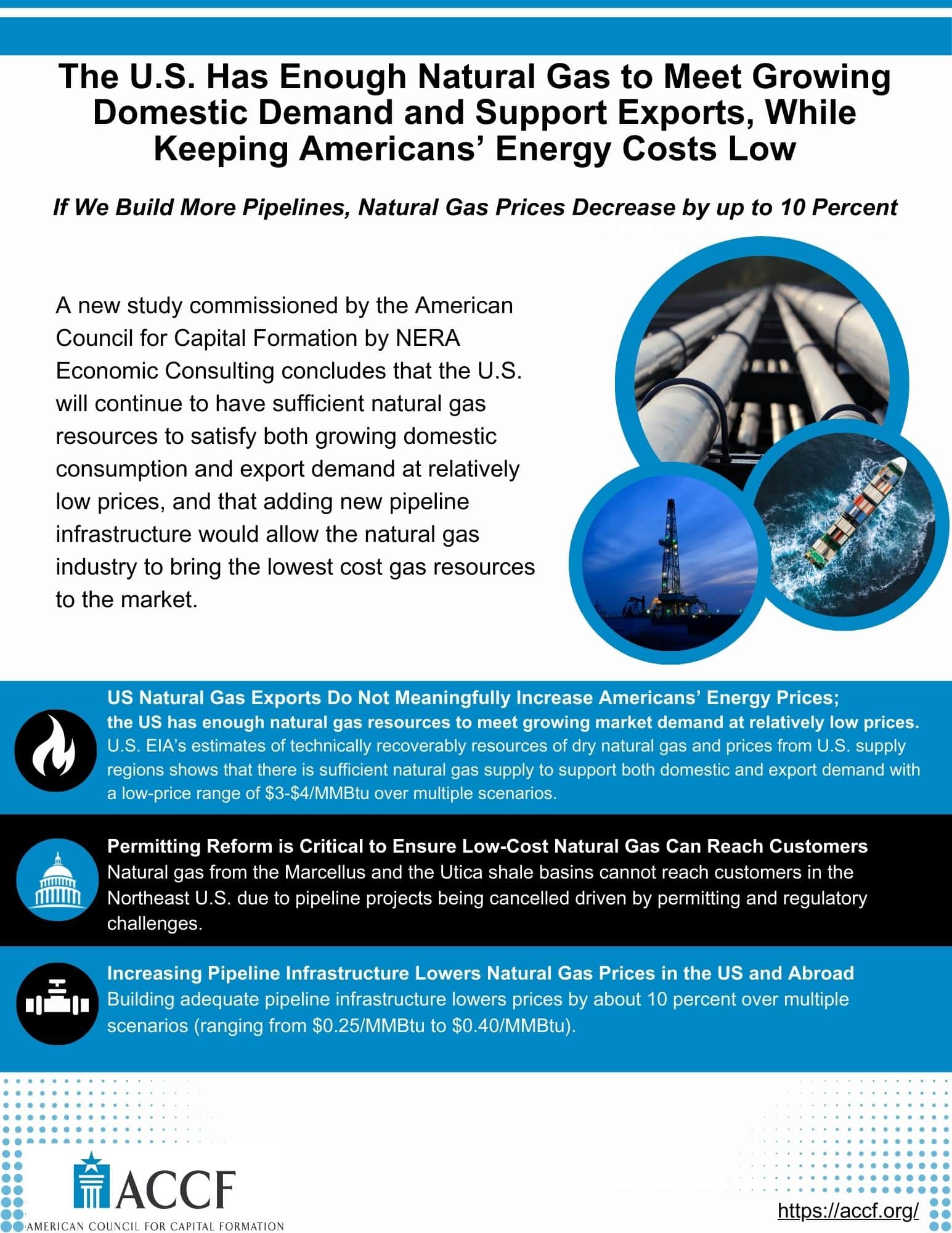

Washington, DC – The U.S. natural gas market remains robust and can satisfy both growing domestic consumption and export demand at relatively low prices, and those prices can be even lower if policymakers ease permitting delays on pipeline infrastructure, according to a new study released today by the American Council for Capital Formation Center for Policy Research (ACCF-CPR). The study, “Analysis of U.S. Natural Gas Market Price Impacts from Increasing Natural Gas Supply Accessibility for Different Natural Gas Demand Outlooks”, evaluates the potential natural gas market price impacts of increasing natural gas supply accessibility for various demand (U.S. LNG exports and domestic demand) outlooks. The report was prepared by global firm NERA Economic Consulting.

“Despite recent global economic turmoil brought about by global crises including the COVID-19 pandemic and the Ukraine-Russia war, the U.S. natural gas supply remains strong,” said ACCF Senior Vice President for Regulatory and Energy Policy Kyle Isakower. “The U.S. can support global exports and meet domestic consumer demand while keeping costs low. The key is streamlining the permitting process to build more pipelines so the industry can bring ample naturalgas resources to market.”

Key takeaways from the study:

- The U.S. continues to have sufficient natural gas resources to meet growing market needs at relatively low prices. An analysis of the U.S. EIA’s estimates of technically recoverable resources of dry natural gas and prices from U.S. supply regions shows that there are sufficient natural gas supply resources to support both domestic and export demand within a reasonably low-price range of $3 to $4/MMBtu (assuming no regional pipeline constraints).

- Lack of new natural gas pipeline infrastructure is a material impediment to bringing the lowest cost gas resources to the market. The lack of new pipeline infrastructure already has likely contributed to sub-optimal current natural gas market conditions and price formation. As a result, the U.S. is unable to utilize the lowest cost natural gas resources from the Northeast region (and particularly from the Marcellus and Utica shale gas basins). Several pipeline projects in the Northeast have been cancelled since 2020 largely as a consequence of regulatory and permitting challenges (See Table 4). In the absence of these infrastructure pipe- line cancellations, natural gas consumers would likely face less upward price pressure and have access to lower cost natural gas supplies which in turn would ultimately lead to lower domestic natural gas prices.

- Natural gas price impacts from expanding pipeline infrastructure are expected to reduce natural gas prices, even with higher levels of U.S. LNG exports. The natural gas price reductions from an expansion in pipe- line infrastructure accessibility are estimated to be between $0.25 and $0.30/MMBtu in 2025 and between $0.25 and $0.40/ MMBtu in 2035 across the numerous scenarios analyzed, see Table 3.

“Contrary to suggestions from some elected officials that exporting natural gas via ship as liquified natural gas (LNG) could cause domestic price increases, this report suggests that under the right policies, the U.S. has ample resources to meet the high demand for natural gas for our global export partners and for the U.S to heat our homes, fuel manufacturing, and importantly, to generate electricity,” Isakower concluded.

Study Resources for “Analysis of U.S. Natural Gas Market Price Impacts from Increasing Natural Gas Supply Accessibility for Different Natural Gas Demand Outlooks”:

READ SUMMARY REPORT REPORT INFOGRAPHIC READ FULL NERA REPORT

{kind=link}